September 18, 2025

September 10, 2025

July 3, 2025

January 10, 2025

Income Tax for Foreign Company: Tax Slabs, Forms & Deductions – 2026

Author

Shoonya Team

Foreign companies earning income from India may be liable to tax in India depending on the nature of income, business connection, treaty position, and whether the income is received, deemed to accrue, or arises in India. For periods beginning on or after 1 April 2026, foreign-company taxation should be read in line with the Income-tax Act, 2025, and the Income-tax Rules, 2026.

Understanding the applicable tax rate, surcharge, cess, return form, and updated compliance structure is essential for accurate filing and tax planning.

What is a Foreign Company under Income Tax?

A foreign company is a company that is not registered in India but earns income from sources within India.

Under the Income Tax Act, a company is classified as a foreign company if:

- It is incorporated outside India

- Its control and management are situated outside India

- It earns income that is received, accrued, or deemed to accrue in India

Income Tax Rate for Foreign Company in India (AY 2026–27)

Income tax for domestic companies and foreign companies differs in India. The applicable foreign company tax rate in India is as follows:

| Condition | Income Tax Rate for Foreign Company |

| Royalty or Fees for Technical Services received from the Government of India or an Indian concern under an approved agreement between 1st April 1961 and 1st April 1976 | 50% |

| Any other income | 35% |

Do Foreign Companies Have Tax Slabs?

No. Foreign companies are generally taxed at specified flat rates, not slab-based rates like individuals. Their final tax liability may vary based on the type of income, surcharge, cess, and treaty position.

Foreign Company Income Tax Surcharge, Marginal Relief, and Health & Education Cess

- Surcharge: 2% where total income exceeds ₹1 crore but does not exceed ₹10 crore

- Surcharge: 5% where total income exceeds ₹10 crore

- Marginal relief: available so that the additional tax payable due to surcharge does not exceed the income exceeding the threshold

- Health and education cess: 4% on tax plus surcharge

Tax Deduction for Foreign Company- FY 2025-26

Foreign companies can benefit from deductions under Chapter VI-A of the Income Tax Act:

1. Section 80G – Donations to Charitable Funds

- Eligibility: Contributions to prescribed charitable institutions.

- Deduction Limits:

- 100% deduction for eligible donations.

- 50% deduction for certain donations.

- Condition: No cash donations above ₹2,000 allowed.

2. Section 80GGA – Donations for Scientific Research and Rural Development

- Eligibility: Contributions to approved research associations and rural development projects.

- Condition: No cash donations above ₹2,000 allowed.

3. Section 80GGC – Contributions to Political Parties

- Eligibility: Donations made to political parties or electoral trusts.

- Condition: Only non-cash contributions qualify for deduction.

4. Section 80IAB – Profits from Special Economic Zones (SEZs)

- Eligibility: Companies engaged in SEZ development.

- Deduction: 100% of profits for 10 consecutive years within the first 15 years from SEZ notification.

- Condition: No deduction if SEZ development begins after April 1, 2017.

5. Section 80IE – Profits from North-Eastern States

- Eligibility: Companies operating in the North-Eastern states.

- Deduction: 100% of profits for 10 years.

6. Section 80JJAA – Deduction for New Employment

- Eligibility: Companies subject to tax audit under Section 44AB.

- Deduction: 30% of additional employee cost for three years.

7. Section 80LA – Offshore Banking Units & International Financial Services Centre (IFSC)

- Eligibility: Banking units in SEZs/IFSCs.

- Deduction: 100% of specified income for 5 consecutive years.

Return Forms and Compliance Documents for Foreign Companies

Foreign companies may need to use different return forms, certificates, and compliance reports depending on the nature of income, audit requirements, TDS reporting, and treaty claims. Under the Income-tax Rules, 2026, several familiar forms have been renumbered.

1. ITR-6

The Income Tax Department’s return-applicable guidance continues to point companies other than those claiming exemption under section 11 to ITR-6. Foreign companies filing a company return in India should check the latest portal instructions before filing.

2. Form 26AS (Annual Information Statement – AIS)

- Provided by: Income Tax Department (Available on e-Filing Portal: Login > e-File > Income Tax Return > View Form 26AS).

- Includes:

- Tax Deducted/Collected at Source (TDS/TCS)

- Specified Financial Transactions (SFT) information

- Advance Tax payments

- Demand/Refund details

- GST and foreign government-reported information

3. Form 16A

- Issued by: Deductor to Deductee

- Purpose: Certificate of TDS on income other than salary.

- Includes:

- Amount of TDS

- Nature of payments

- TDS deposited with the Income Tax Department

4. Form 3CA-3CD

- Applicable for: Foreign companies requiring a mandatory tax audit under Section 44AB.

- Purpose: Report of audit of accounts and particulars of income.

- Due Date: One month before the due date for filing the income tax return under Section 139(1).

5. Form 3CE

- Applicable for: Non-resident taxpayers receiving royalty or technical service fees from the Government of India or an Indian concern.

- Purpose: Report from an accountant under Section 44DA, submitted one month before the tax return filing due date.

6. Form 29B

- Applicable for: Foreign companies subject to Minimum Alternate Tax (MAT) under Section 115JB.

- Purpose: Certification of book profit computation.

- Due Date: One month before the tax return filing deadline.

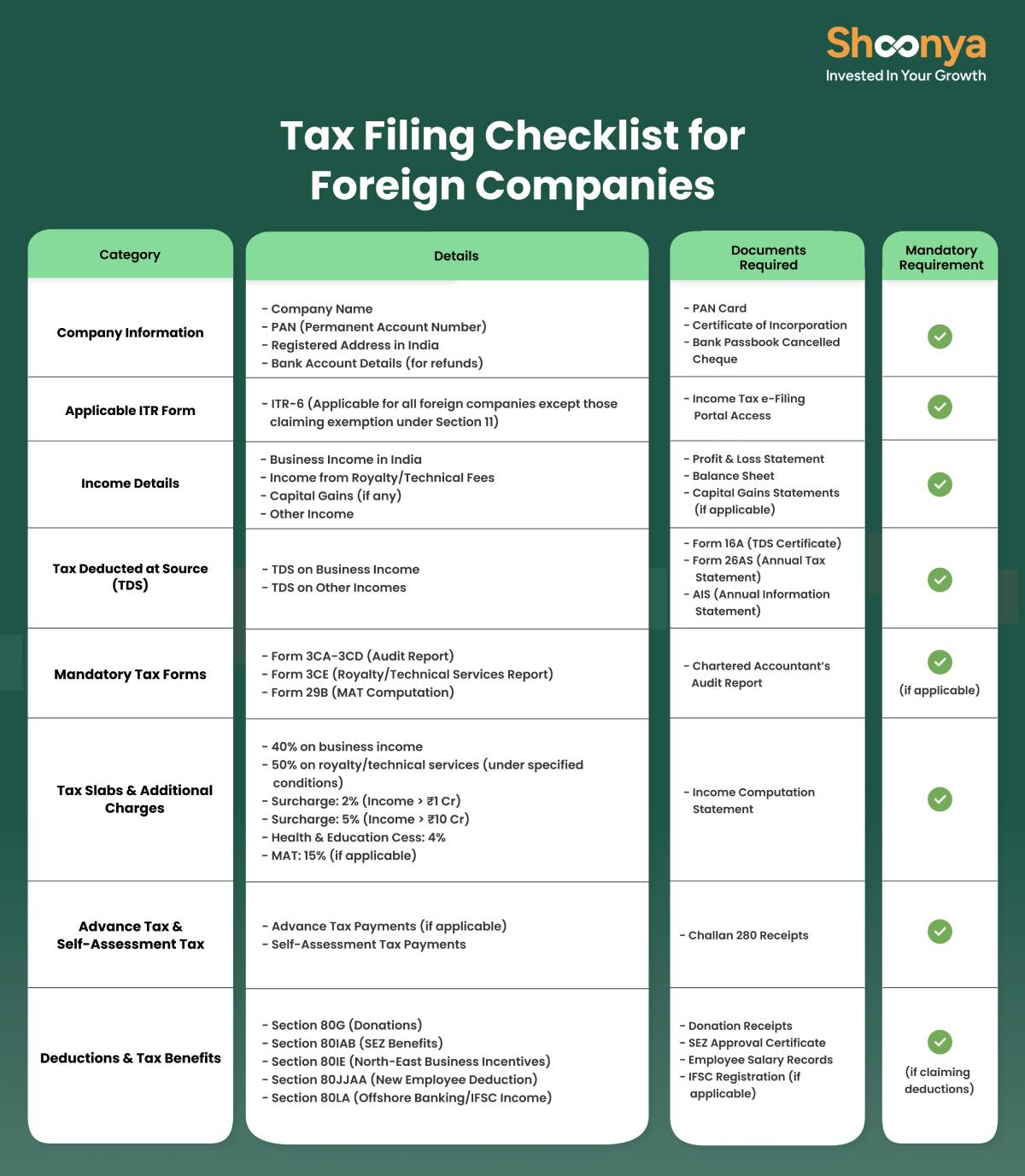

ITR Filing Checklist for Foreign Company

Before you begin filing your ITR for a foreign company, you have to make sure you have all the necessary documents and details ready. Here is a quick checklist to help you stay organised and avoid mistakes.

AY vs Tax Year: What Changes from 1 April 2026?

This distinction is important while updating tax content for 2026. Income earned from 1 April 2025 to 31 March 2026 continues to be governed by the earlier law and assessed in AY 2026-27. Income earned from 1 April 2026 onwards falls under the new framework and is referred to as Tax Year 2026-27.

So, if this blog is meant to explain the new rules effective from 1 April 2026, it should primarily use Tax Year 2026-27 rather than AY 2026-27.

How to File ITR for a Foreign Company

To comply with tax laws, foreign company tax filings must be submitted via the e-Filing portal of the Income Tax Department using ITR-6.

Step-by-Step Guide for Foreign Company Tax Filing:

- Register on the e-Filing Portal

- Visit Income Tax India e-Filing and create an account.

- Use the PAN of the foreign company to register.

- Log in and Choose the Correct ITR Form

- Select ITR-6 (for companies that do not claim exemption under Section 11).

- Pre-fill Data

- Retrieve the relevant tax credits, TDS details, and information available through the applicable annual information statement framework and supporting tax records before filing.

- Enter Financial Details

- Fill in all sources of income, including royalty, foreign income tax, and income tax on foreign investment.

- Claim Deductions for Foreign Companies

- Foreign companies can claim income tax deductions for foreign companies under various sections (e.g., Section 80G, 80IAB, 80IE, 80JJAA, and 80LA).

- Calculate Tax Liability

- Compute tax liability after considering the applicable base rate, surcharge, cess, treaty position, and any eligible deductions.

- Pay Taxes & File the ITR

- Pay any pending taxes online and submit the return.

- E-Verify the Return

- Complete verification using the mode permitted for the company return on the e-filing portal, such as a digital signature, where applicable.

What are the Benefits of Filing ITR for a Foreign Company

Filing ITR for foreign companies provides multiple advantages, including:

- Compliance & Avoiding Penalties: Filing ITR ensures compliance with Indian tax laws and helps foreign companies avoid hefty fines and legal issues.

- Tax Deductions & Savings: Foreign companies can claim deductions under various sections.

- Ease of Business Operations: Proper tax filing helps ensure smooth business transactions, secure regulatory approvals, and maintain credibility.

- Avoiding Legal Complications: Timely ITR filing prevents tax disputes, audits, and restrictions on repatriating profits from India.

What are the Common Mistakes to Avoid in Tax Filing for Foreign Companies

Here are some common mistakes and their consequences:

- Using outdated tax rates: The general rate for foreign companies should not be stated as 40% in a 2026 update when the current official guidance shows 35% for other income.

- Mixing AY and Tax Year references: A 2026 rules article should clearly distinguish old-law AY 2026-27 content from new-law Tax Year 2026-27 content.

- Using old form numbers without noting renumbering: Under the Income-tax Rules, 2026, several commonly used forms have been renumbered.

- Incorrect treaty or surcharge computation: Foreign-company tax liability may change based on surcharge, cess, and DTAA position.

- Overstating MAT applicability: MAT should not be presented as universally applicable to all foreign companies without qualification.

Conclusion

Tax compliance for foreign companies in India is no longer just about knowing the tax rate. From 1 April 2026, businesses also need to align with the new tax-year framework, updated form numbering, and the revised compliance structure under the Income-tax Rules, 2026. Using the correct tax rate, surcharge, return form, and disclosure approach is essential for accurate filing and smoother compliance.

Income Tax for Foreign Companies: FAQs

Yes, foreign companies earning income in India are subject to income tax. The tax rate is typically 40%, with additional surcharges and cess as applicable.

Foreign companies are generally taxed at 35% on other income, while certain specified old royalty or technical service agreements may attract 50% tax. Surcharge and 4% cess apply where relevant.

Foreign companies are taxed at 40% on their total income, with a 50% tax on royalties and technical service fees under specified agreements.

The 2026 tax changes include revised slabs, surcharge rates, and deductions. Check the latest Income Tax Act amendments for exact details.

Yes, TDS is deducted on payments made to foreign companies for services like royalties, technical fees, and dividends, as per the applicable tax treaties.

No, foreign companies are generally taxed at specified flat rates rather than slab-based rates.

Yes. A surcharge of 2% applies where total income exceeds ₹1 crore but does not exceed ₹10 crore, and 5% applies above ₹10 crore, subject to marginal relief.

Domestic companies pay 22-30% tax under different schemes, while foreign companies are taxed at 40%, plus surcharges and cess.

The corporate tax rate depends on company type; domestic companies pay between 22%-30%, whereas foreign companies pay 40%, plus applicable surcharges.

Foreign companies are taxed at 40% on general income and 50% on specific royalties or fees for technical services under certain agreements.

Source- Incometax.gov.in

Disclaimer: This content is for education and awareness purposes only and should not be considered investment advice or a recommendation. Investments in securities markets are subject to market risks. Read all the related documents carefully before investing.

Explore Our Offerings

Stocks

Trade equities across NSE and BSE with zero delivery charges. Invest, hold or sell with a seamless experience.

Future & Options

Execute complex strategies with simple tools and real-time data.

IPOs

Apply to the latest IPOs in just a few taps. Stay updated and capture opportunities as they open.