September 18, 2025

September 10, 2025

July 3, 2025

January 10, 2025

How to Make a Cancelled Cheque – Learn with a Cancelled Cheque Sample

Author

Shoonya Team

Have you ever issued a cheque to someone and then regretted it? Maybe you made a mistake in writing the cheque, or you changed your mind about the payment, or you suspected some fraud. Or maybe you just needed to prove that you have a bank account for some reason. In any of these cases, you would need a cancelled cheque.

In this blog, we will explain how to cancel a cheque, along with a cancelled cheque sample!

What is a Cancelled Cheque?

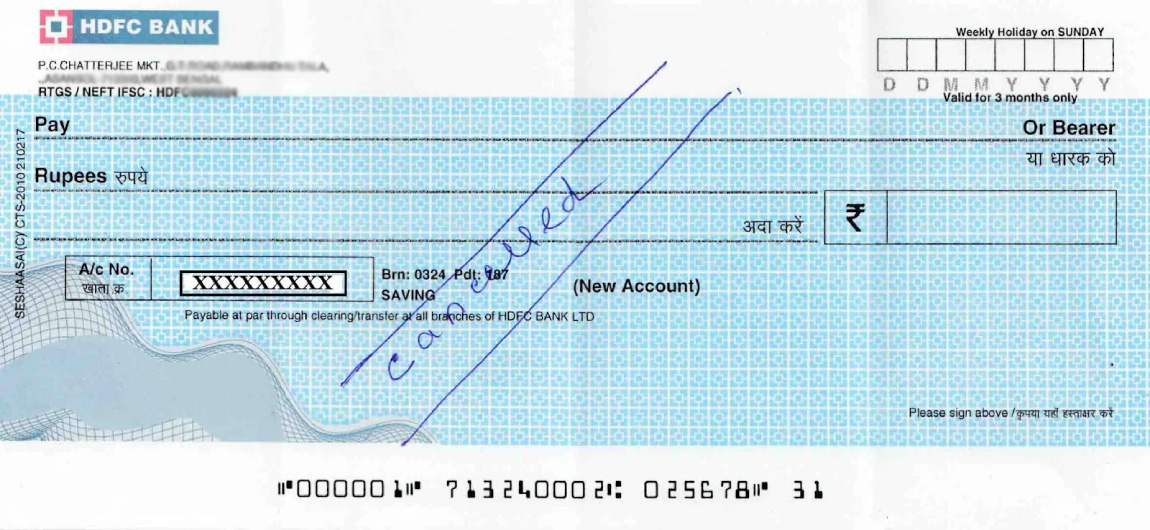

A cancelled cheque is usually represented as one that has two parallel lines drawn across it, followed by the word “cancelled” written between them. It is also known as a crossed cheque or a payee account cheque.

- A cancelled cheque cannot be used to withdraw or transfer money.

However, it can be used to verify your bank account details, such as your name, account number, IFSC code, and MICR code.

- A cancelled cheque acts as proof of your banking identity and prevents any misuse of your cheque.

A cancelled cheque leaf is a cheque with “CANCELLED” written across it in large, capital letters between two parallel lines, which deactivates it for payment while serving as a safe way to provide proof of your bank account details, such as your account number, IFSC code, and MICR code.

Cancelled Cheque Example

Check out this cancelled cheque image-

How to Make a Cancelled Cheque?

Wondering how to cancel a cheque?

You just need to follow these steps:

• Select a new cheque from your chequebook.

• Draw two parallel lines diagonally across the cheque.

• Write the word “CANCELLED” in clear, bold, capital letters between the lines.

• Do not sign the cheque or fill in the date, payee name, or amount.

• Ensure the account number, IFSC code, MICR code, bank name and branch details remain visible.

What Ink to Use on Cheques?

You must always use blue or black ink for clarity.

What is a Cancelled Cheque Used For?

A cancelled cheque cannot be used to withdraw money, which makes it safe to share bank details.

1. Verification of bank account details

It is used to verify that you hold an active bank account and to provide accurate details such as account number, bank name, IFSC code and MICR code.

Banks, NBFCs and financial institutions request it when you open an account, apply for a loan or set up fund transfers.

2. KYC completion for investments

A cancelled cheque is also required during Know Your Customer procedures for mutual funds, stock market accounts and other financial schemes. It confirms the authenticity of your bank account and securely links your account to your investment profile.

Now, choose from more than 3000 mutual fund options and start investing with a free demat account. Open your account today.

3. EPF withdrawal

A cancelled cheque needs to be submitted as compulsory proof of bank account details when you are withdrawing money from the Employee Provident Fund account. It ensures that the withdrawn amount is transferred to the correct bank account.

Know About – How to Check PF Claim Status Online

4. Automatic bill payments

You have to provide a cancelled cheque to authorise recurring payment arrangements for electricity bills, mobile bills, insurance premiums or subscription services. It confirms that the company can debit your account for regular payments.

5. Equated Monthly Instalments (EMIs)

It is also needed for activating EMIs for loans or credit facilities from banks and NBFCs. A cancelled cheque allows lenders to directly debit the instalment amount from your account on the scheduled date.

6. Electronic Clearance Service activation

It is necessary to activate the Electronic Clearance Service facility for smooth and secure fund transfers. The cancelled cheque acts as proof of your account details for the institution initiating the debit.

7. Demat account opening

Essential for opening a Demat account used for trading in shares and securities. It verifies that you possess an active bank account and helps facilitate smooth fund transfers during trading.

8. Insurance-related transactions

This has to be submitted while purchasing insurance policies or updating existing ones. It verifies your bank account for premium payments, refunds or claim settlements.

Risks Associated with Cancelled Cheques

While cancelled checks are ineffective for fund withdrawals, they pose a risk of cyber theft or misuse.

But just because it can’t be used for transactions doesn’t mean you should leave it lying around.

- Identity theft and unauthorised account use

Sensitive details on a cancelled cheque can allow a fraudster to attempt to open new accounts in your name or commit financial fraud. Even though the cheque cannot be used for payment, weak security can still expose your account number to unauthorised digital transactions.

- Data breaches

Organisations that store your cancelled cheque for verification may still face cyber incidents that expose your banking details. Even trusted third parties are vulnerable to leaks, putting your personal and financial information at risk.

- Misuse by trusted individuals

Sharing a cancelled cheque with someone you know does not remove the risk of them misusing your account information.

If handled carelessly, anyone with access can attempt unauthorised activity using the visible account details.

- Fraudulent alteration

A fraudster may try to alter details on a cancelled cheque to create unauthorised versions for manipulation. Forged or counterfeit cheques created from the original may be used to mislead banks or financial institutions.

How to Mitigate Cancelled Cheque Risks Effectively

Most risks that come with a cancelled cheque can be avoided if you handle it with a little more care than people usually think it needs.

• You should always share a cancelled cheque only with trusted institutions to prevent exposure of sensitive details.

• Avoid sharing scanned copies online or through unsecured channels.

• You need to keep a check on your bank statements regularly to detect any unusual activity early.

• Inform your bank immediately if a cancelled cheque is lost or misplaced.

• Destroy any cancelled cheque securely once it is no longer required.

What Should I Do If I Lost My Cancelled Cheque

What to do immediately

- Contact your bank at once so they can monitor your account for any suspicious activity.

- Notify the institution that requested the cancelled cheque so they are aware of the loss.

- Request a new cancelled cheque if needed, and keep a proper record of the replacement.

Why is this important?

- A cancelled cheque contains sensitive information such as your account number, IFSC code, and bank details.

- These details can still be misused for fraudulent activity or unauthorised digital transfers.

- The presence of your personal information increases the risk of identity theft.

Cancelled Cheque vs. Stop Payment: What’s the Difference?

These two terms may sound similar, but there is a difference between a cancelled cheque and the stop payment feature.

- Cancelled Cheque: It’s a cheque with lines drawn and ‘CANCELLED’ written on it. It can’t be used to withdraw money, but it shows your bank details.

- Stop Payment: This is a request made to the bank not to process a cheque that you have issued. It’s used when you want to prevent the cheque from being cashed.

There might be a fee for this service, and you typically need to provide the bank with details like the cheque number, the date of issue, and the amount.

Conclusion

Understanding a cancelled cheque and how to write a cancelled cheque is important. Whether it’s completing KYC requirements, facilitating EPF withdrawals, or opening a Demat account, a cancelled cheque continues to serve an important purpose in most formal processes.

However, you should be careful and remember your cancelled cheque details.

How to Cancel a Cheque – FAQs

A cancelled cheque is a cheque on which two parallel lines are drawn and the word cancelled is written across it. It is used only for verification of bank details and cannot be used for payments.

It is generally safe when shared with trusted institutions for formal verification. However, it still contains sensitive information, so it must be handled carefully.

A signature is not required on a cancelled cheque because it is not meant for any transaction. Only the parallel lines and the word cancelled are needed.

A cancelled cheque confirms your bank account details such as account number, bank name, and IFSC code. It acts as proof of ownership without allowing any direct withdrawal or payment.

No, a cancelled cheque does not require a signature. A cancelled cheque is a cheque that has two parallel lines drawn across it and the word “cancelled” written between them.

To draw a cancelled cheque, cross it with two parallel lines and write ‘CANCELLED’ across it, making sure not to alter/hide the account details.

A cancelled cheque cannot bounce because it is not valid for any financial transaction and cannot be presented to a bank for payment.

Banks, financial institutions, employers, mutual fund companies, and EPF offices often request a cancelled cheque for verification of your bank account details.

Disclaimer: Investments in the securities market are subject to market risks; read all the related documents carefully before investing.

Explore Our Offerings

Stocks

Trade equities across NSE and BSE with zero delivery charges. Invest, hold or sell with a seamless experience.

Future & Options

Execute complex strategies with simple tools and real-time data.

IPOs

Apply to the latest IPOs in just a few taps. Stay updated and capture opportunities as they open.