September 18, 2025

September 10, 2025

July 3, 2025

January 10, 2025

HUF Income Tax Slabs FY 2025–26 (AY 2026–27): Deductions, Benefits and ITR Rules

Author

Shoonya Team

Many taxpayers overlook one of the most effective ways to manage family income and reduce tax liability: forming a HUF.

Under income tax laws, an HUF is treated as a separate legal entity, which means it can earn income, claim deductions, and be taxed independently. This allows families to split income across members and optimise overall tax outflow.

For FY 2025–26 (AY 2026–27), HUF income tax slabs follow the same taxation rules, with the option to choose between the old and new tax regimes to ensure compliance and make full use of its tax benefits.

What is the Hindu Undivided Family in Income Tax?

HUF’s full form is Hindu Undivided Family. For tax purposes, an HUF is recognised as a separate taxable person. It may hold property, earn income, claim eligible deductions, and file a separate return.

In practice, HUF taxation is relevant where there is joint family property, ancestral assets, or income that belongs to the family unit rather than an individual member.

How is an HUF Recognised for Tax Purposes?

An HUF is not created by a simple contract. For tax purposes, separate assessment generally becomes relevant when there is joint family property, ancestral assets, or income that belongs to the HUF and not to an individual member.

To support separate tax treatment, the HUF usually needs its own PAN, bank account, and records of income and assets.

1. Existence of Coparcenership

Coparceners are those relatives who, through birth, have a claim over components of a joint family property. The 2005 amendment gave daughters an equal right as their brothers over the family property; it made them coparceners too. Daughters were brought into the fold of coparceners and now have claims over family property, as do sons. Once considered the income of an HUF, unless partitioned by a coparcener, the income of a family will continue as such.

2. Presence of Joint Family Property

For an HUF to be taxed separately, it must own joint family property, which includes:

- Ancestral Property: Property inherited from the father, grandfather, or great-grandfather.

- Property Acquired Using Ancestral Funds: Any assets or investments made using ancestral wealth.

- Property Transferred by Family Members: If a family member transfers property to the HUF, the income generated from it will be taxed as HUF income.

Who Can Form a Hindu Undivided Family (HUF)?

An HUF can exist in various family structures. It is not restricted to large joint families and can be formed even with a small group of related members.

Examples of valid HUF structures include:

- Family of a husband and wife (even without children)

- Family of two widows of deceased brothers

- Family of two or more brothers

- Family of an uncle and nephew

- Family of a mother, son, and son’s wife

- Family of a male and his late brother’s wife

Exception

- When a daughter inherits ancestral property, it is treated as her individual property.

- Any income generated from such property is taxed in her individual capacity, not as HUF income.

- This rule also applies to any legal heir inheriting property from an HUF

Note: The role of Karta is not restricted to male members. Eligibility depends on coparcenary rights and seniority within the HUF. Want to know if daughter and daughter-in-law can be Karta of HUF?

Latest Updates of HUF Income Tax Slab for the AY 2026-27

HUFs continue to follow the slab structure applicable to individuals under the relevant regime. Under the revised default regime applicable for AY 2026-27 and carried into the new framework, the slab rates begin at nil up to ₹4 lakh and rise gradually to 30% above ₹24 lakh. HUFs can also opt for the old regime, subject to the applicable conditions.

HUF Income Tax Slabs for AY 2026-27

| Annual Income | Income Tax Rate |

| Upto ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

What is HUF Income Tax & How is HUF Taxed?

A Hindu Undivided Family (HUF) is treated as a separate taxable entity under the Income Tax Act, 1961, and its income is taxed independently from its members.

Taxation and Deductions

- HUF is taxed at the income tax slab rates applicable to individuals

- It can claim deductions under Section 80C, Section 80D, and other applicable provisions

Insurance Premiums

- HUF can purchase life insurance policies for its members

- Premiums paid are eligible for deduction under applicable sections

Salary Paid to Members

- Members actively involved in managing the HUF can receive a salary

- Such payments are treated as a business expense, reducing the taxable income of the HUF

Investment Income

- HUF can invest in shares, mutual funds, fixed deposits, and other financial instruments

- Income such as interest, dividends, and capital gains is taxed in the hands of the HUF.

Tax Slabs for AY 2026-27: Old Tax Regime vs New Tax Regime for HUF

When it comes to taxation, Hindu Undivided Families (HUFs) have the option to choose between the old tax regime and the new tax regime, just like individuals. The primary distinction between the two lies in the availability of deductions and exemptions. HUFs can choose between the old and default regimes, but the choice should be based on deductions claimed, type of income, and whether the HUF has business or professional income.

Old Tax Regime (With Deductions)

| Annual Income | Tax Rate |

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Old Tax Regime vs New Tax Regime for HUF (AY 2026–27)

| Particulars | Old Tax Regime | New Tax Regime (Default) |

| Tax Rates | Higher slab rates | Lower slab rates |

| Basic Exemption Limit | ₹2,50,000 | ₹4,00,000 |

| Deductions (80C, 80D, etc.) | Allowed | Not allowed (except limited cases like 80CCD(2)) |

| Rebate under Section 87A | Not available to HUF | Not available to HUF |

| Standard Deduction | Not applicable for HUF | Not applicable for HUF |

| Investment Benefits | Available (PPF, LIC, ELSS, etc.) | Not available |

| Complexity | Higher due to multiple deductions | Lower due to simplified structure |

| Suitability | Better for those with high deductions | Better for those with fewer deductions |

Which Tax Regime Should an HUF Choose?

The old regime may be more suitable where the HUF claims substantial deductions such as section 80C, 80D, or housing-related benefits. The default regime may be simpler where deductions are limited and the HUF wants lower slab rates without tracking multiple exemptions.

Important: If the HUF has business or professional income, switching between regimes is restricted and should be evaluated carefully before exercising the option.

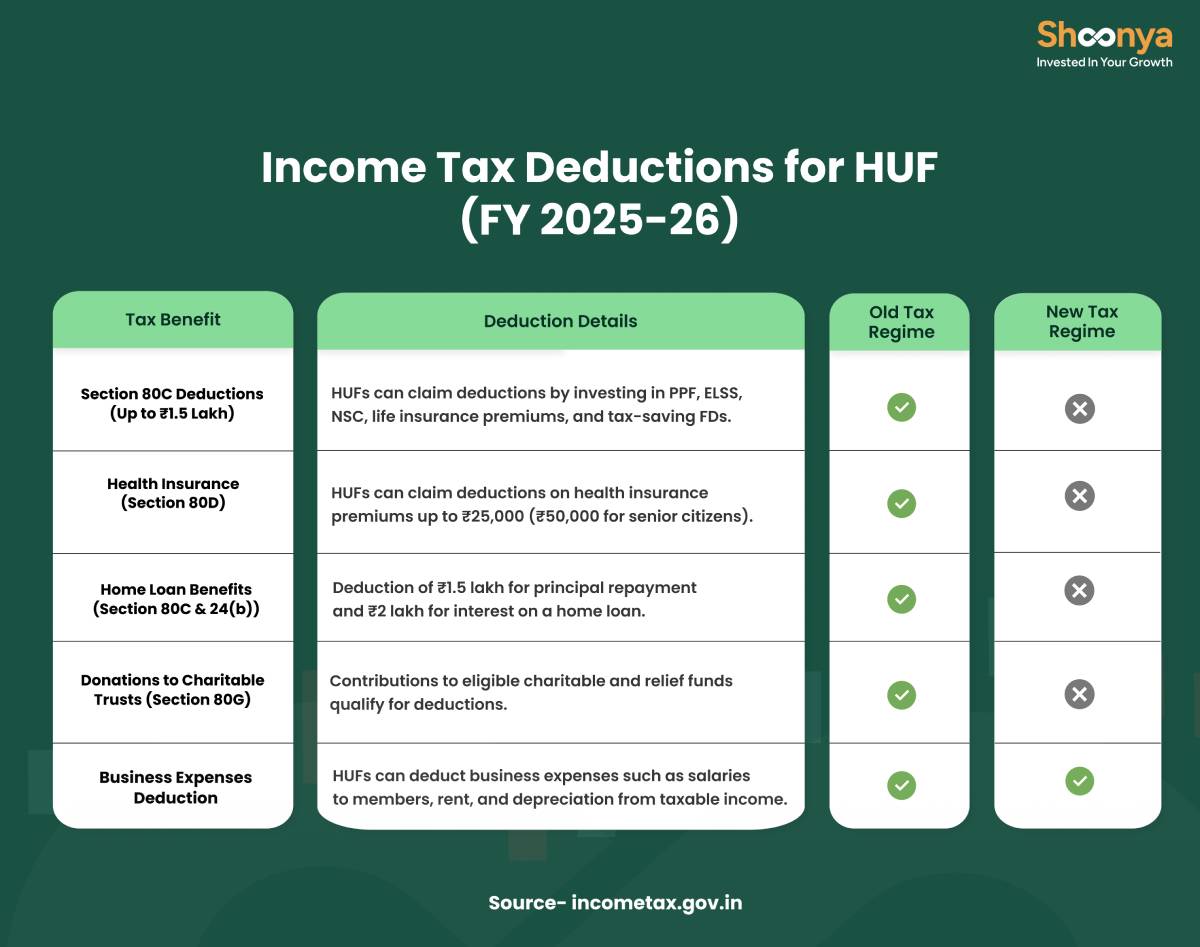

Income Tax Deductions for HUF (FY 2025-26)

Since an HUF is taxed separately, it may claim eligible deductions in its own return, subject to the conditions of each section. These deductions can help reduce taxable income where the HUF has qualifying investments, expenses, or property-related payments.

Let us understand how an HUF can reduce its tax liability with a practical example.

Mr Amit Verma decides to create an HUF with his wife, son, and daughter as members. He has a salary income of ₹25 lakh per year, and the HUF owns a commercial property inherited from his father, which earns an annual rental income of ₹9 lakh. By forming an HUF, Mr. Verma can legally split the income and claim additional deductions, leading to substantial tax savings.

| Income from Various Sources | Before HUF Formation (Individual’s Return) | After HUF Formation (Mr Verma’s Return) | HUF’s Return |

| A) Salary Income | ₹25,00,000 | ₹25,00,000 | – |

| B) Rental Income from Property | ₹9,00,000 | ₹9,00,000 | |

| C) Standard Deduction on House Property (30% of ₹9,00,000) | (₹2,70,000) | (₹2,70,000) | |

| D) Taxable Rental Income (B – C) | ₹6,30,000 | ₹6,30,000 | |

| Total Taxable Income (A + D) | ₹31,30,000 | ₹25,00,000 | ₹6,30,000 |

| E) Section 80C Deduction | ₹1,50,000 | ₹1,50,000 | ₹1,50,000 |

| Net Taxable Income (D – E) | ₹29,80,000 | ₹23,50,000 | ₹4,80,000 |

| Tax Payable (As per Old Regime + 4% Cess) | ₹7,02,600 | ₹5,20,200 | ₹10,400 |

| Total Tax Paid (Before HUF) | ₹7,02,600 | ||

| Total Tax Paid (After HUF Formation) | ₹5,30,600 | ||

| Tax Saved by Forming an HUF | ₹1,72,000 |

How HUF Helped in Tax Savings?

- Rental income was transferred to the HUF, reducing Mr Verma’s individual taxable income.

- Both Mr Verma and HUF claimed Section 80C deductions separately, lowering taxable income.

- The HUF paid tax on its income separately, benefiting from lower slab rates.

- By forming an HUF, Mr Verma legally saved ₹1,72,000 in taxes.

ITR Forms for Hindu Undivided Family for AY 2026-27

The applicable return form depends on whether the HUF has business income, presumptive income, or only non-business income. The Income Tax Department’s return-applicable page for HUF confirms the broad use of ITR-2, ITR-3, and ITR-4.

Here’s a simplified breakdown of applicable returns for HUF tax filing:

1. ITR-2 Use ITR-2 if the HUF does not have income under the head “Profits and Gains of Business or Profession.

2. ITR-3: Use ITR-3 if the HUF has business or professional income.

3. ITR-4 (Sugam): ITR-4 can be used by a resident HUF with total income up to ₹50 lakh where business or professional income is offered under the presumptive scheme, subject to the eligibility conditions and exclusions prescribed by the department.

*ITR-4 Not Applicable If:

- The HUF’s total income exceeds ₹50 lakh.

- The HUF has a company directorship or holds unlisted equity shares.

- The HUF has foreign assets, foreign income, or signing authority in a foreign account.

- Deferred ESOP tax or brought forward losses exist.

Key Income Tax Forms & Their Purpose for HUF Taxation

| Form | Provided/Submitted By | Purpose & Details |

| Form 16A | Deductor to Deductee | TDS certificate for income other than salary. Shows TDS amount, nature of payment, and TDS deposited with the Income Tax Department. |

| Form 26AS | Income Tax Department | Available on e-Filing Portal (Login > e-File > View Form 26AS). Shows TDS/TCS, tax payments, demand/refund status, and additional financial information. |

| AIS (Annual Information Statement) | Income Tax Department | Accessed via Income Tax e-Filing Portal (Login > e-File > AIS). Includes TDS/TCS, SFT transactions, tax payments, refunds, GST details, and foreign-reported data. |

| Form 15G | Resident Individual (< 60 years), HUF, or Other Non-Corporate Entities | Declaration to banks for non-deduction of TDS on interest income if the total income is below the basic exemption limit. |

| Form 67 | Taxpayer | Statement for income earned outside India and claiming Foreign Tax Credit. Must be filed before the ITR due date (u/s 139(1)). |

| Form 3CB-3CD | Taxpayer (if audit required u/s 44AB) | Audit report & financial statement details for taxpayers subject to tax audit. Must be filed one month before the ITR due date. |

| Form 3CEB | Taxpayer (if involved in international or specified domestic transactions) | Report from a Chartered Accountant on cross-border or specified domestic transactions (u/s 92E). Must be filed one month before the ITR due date. |

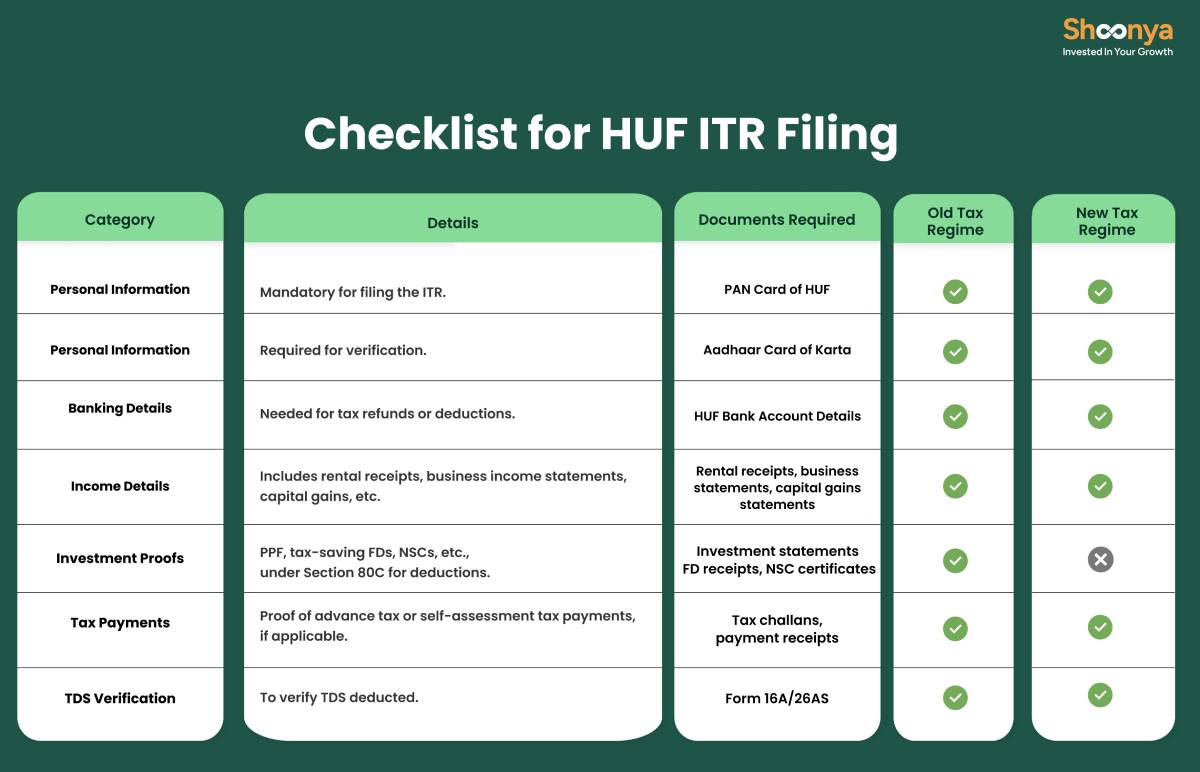

Checklist for HUF ITR Filing

How Do You File an Income Tax Return Online for HUF?

Filing ITR for an HUF is similar to that of individual taxpayers but requires additional steps:

- Log in to the Income Tax e-Filing portal using the PAN of the HUF.

- Choose the correct ITR form based on whether the HUF has business income, presumptive income, or only non-business income.

- Review the pre-filled information and update income details, deductions, tax payments, and bank account details.

- Compute tax liability under the appropriate regime.

- Submit the return and complete e-verification through the permitted method on the portal.

What are the Common Mistakes to Avoid While Filing ITR for HUF?

1. Incorrect Selection of ITR Form: Filing the wrong form (e.g., ITR-1 instead of ITR-2, ITR-3, or ITR-4) can lead to processing delays or rejection.

2. Not Reporting All Incomes: HUFs must disclose all sources of income, including rental income, interest from investments, capital gains, and business income, to avoid scrutiny and penalties.

3. Claiming Deductions Meant for Individuals: Certain deductions like Section 80E (Education Loan Interest) are meant for individuals and cannot be claimed by HUFs.

4. Failing to E-Verify: Filing is incomplete until e-verification is done via Aadhaar OTP, Net Banking, or sending a signed ITR-V to CPC Bengaluru. Unverified returns are treated as not filed.

5. Ignoring Advance Tax Payments: If the HUF’s total tax liability exceeds ₹10,000 in a financial year, advance tax must be paid in instalments (June 15, Sept 15, Dec 15, and March 15) to avoid interest under Section 234B & 234C.

6. Mismatched Bank & PAN Details: Ensure that HUF’s bank account and PAN details are correct to prevent issues in refund processing or tax notices.

Tip: Cross-check all details before filing to avoid notices, penalties, or delayed refunds!

What is Assisted ITR Filing For HUF Taxation

The Income Tax Department has introduced several enhancements on the e-Filing portal to simplify tax filing:

- ITR Selection Wizard: Helps choose the correct ITR form

- Pre-filled ITRs: Reduce manual entry and errors

- Offline Utility: Offers a user-friendly filing experience

- Chatbot & Guides: Provides step-by-step assistance with manuals and videos

- Assisted Filing: Allows taxpayers to seek help from a CA, ERI, or Authorised Representative

Who Can Assist You?

1. Chartered Accountant (CA)

A CA, a qualified professional under ICAI, assists with ITR filing and tax compliance.

- Taxpayers can add, assign, or remove a CA via the ‘My CA’ service on the portal.

2. e-Return Intermediary (ERI)

An ERI is an authorised entity that files ITRs and performs tax-related functions.

- Taxpayers can add, activate, or remove an ERI via the ‘My ERI’ service.

- ERIs can also register taxpayers and add them as clients with consent.

3. Authorised Representative (AR)

An Authorised Representative (AR) acts on behalf of taxpayers in specific situations.

| Taxpayer Type | Reason for Appointment | Authorized Person |

| Individual | Absent from India | Resident Authorised Person |

| Individual | Non-Resident | Resident Agent |

| Individual | Other reasons | Resident Authorised Person |

| Company (Foreign Entity) | Foreign director without PAN & DSC | Resident Authorised Person |

Taxpayers can assign an AR via the e-Filing portal to manage tax filings on their behalf.

Income Tax Calculator for Quick & Easy Tax Estimation

The Income Tax Calculator helps individuals, professionals, and businesses estimate their tax liabilities based on income, deductions, and tax regimes. The Income Tax Department offers an official calculator on its e-filing portal, allowing users to compare tax liabilities under the Old and New Regimes.

How to Use It?

- Access the Calculator → Visit the e-filing portal > Quick Links > Income and Tax Calculator

- Choose Calculator Type →

- Basic Calculator: Quick estimate based on income and deductions

- Advanced Calculator: Detailed breakdown by income sources, deductions, and TDS/TCS

- Enter Details → Input AY, taxpayer category, income, deductions

- Review Tax Liability → View total tax & interest payable

This tool ensures accurate tax estimation and better financial planning.

What are the Benefits of Filing ITR for HUF?

A Hindu Undivided Family (HUF) provides several tax advantages, making it an effective tool for tax planning and financial management.

1. Separate Taxation: HUF enjoys independent tax treatment, reducing the family’s total tax burden.

2. Tax-Free Wealth Accumulation: Income earned by HUF is taxed separately, allowing savings on personal taxation.

3. Deductions and Exemptions: HUFs can claim various deductions under Sections 80C, 80D, and 80G.

4. Loan Approvals: A properly filed ITR strengthens loan applications for business or property purchases.

5. Avoiding Penalties: Filing ensures compliance with tax laws and prevents legal issues.

Conclusion

HUF taxation can be useful where the family has valid HUF income, property, or investments that are assessable separately. The key is to choose the correct regime, apply the right slab rates, use the correct return form, and keep HUF records separate from members’ individual tax details.

Income Tax Calculation & Filing for HUF Account|FAQs

A Hindu Undivided Family (HUF) is a distinct taxable entity under Indian law consisting of members from a common ancestor, including their spouses and children.

Under the Old Regime, HUFs followed the same slabs as individuals. Under the New Regime, the revised slabs offer higher exemptions and reduced tax rates.

No, HUF accounts are not eligible for Section 80TTB, which provides deductions on interest income for senior citizens. This benefit is exclusively available to individuals aged 60 and above.

HUFs can file ITR-2 (if no business income), ITR-3 (if engaged in business), or ITR-4 (for presumptive taxation).

An HUF account is a separate bank account in the name of the HUF used to manage the family’s income and financial transactions independently from individual members.

Yes, an HUF can claim interest deductions on home loans under Section 24(b) and principal repayment under Section 80C.

An HUF is taxed separately from its members, allowing families to distribute income efficiently and reduce the overall tax burden.

Source: Incometax.gov.in

Disclaimer: This content is for education and awareness purposes only and should not be considered investment advice or a recommendation. Investments in securities markets are subject to market risks. Read all the related documents carefully before investing.

Explore Our Offerings

Stocks

Trade equities across NSE and BSE with zero delivery charges. Invest, hold or sell with a seamless experience.

Future & Options

Execute complex strategies with simple tools and real-time data.

IPOs

Apply to the latest IPOs in just a few taps. Stay updated and capture opportunities as they open.