September 18, 2025

September 10, 2025

July 3, 2025

January 10, 2025

Income Tax for Senior Citizens and Super Senior Citizens: Tax Guide 2025

Author

Shoonya Team

Worried about your parents’ taxes? Let’s discuss some important things related to income tax for senior citizens and super senior citizens!

As our parents age, we want to ensure their financial comfort. But did you know that many senior citizens miss out on tax benefits simply because they are unaware? Whether it’s increased exemption limits, tax saving options for super senior citizens, or special rebates, the income tax for senior citizen system provides many benefits.

If you’re handling your parents’ taxes, this guide will help you understand how to file ITR for Super Senior Citizens and lower their tax liabilities legally!

Importance of Tax Planning and Filing for Senior Citizens

Many retirees in India stick to old tax habits without realising that tax laws have changed to benefit them. Are you making the most of senior citizen tax deductions, higher exemption limits, and lower tax rates?

Retirement Means Freedom—But Not from Taxes!

Here’s How Income Tax for Senior Citizens Works

In India, senior citizens and super senior citizens are classified based on their age for income tax and other benefits:

- Senior Citizens– Individuals aged 60 years or above but below 80 years.

- Super Senior Citizens– Individuals aged 80 years or above.

Tax planning and timely filing of income tax returns are crucial for senior and super senior citizens. Understanding the income tax slab for senior citizens helps in utilising deductions and exemptions effectively, reducing tax liabilities. The senior citizen age for income tax eligibility is 60 years, while the super senior citizen age is 80 years and above, each having different tax slabs.

Latest Updates for the AY 2025-26: Income Tax for Senior Citizens and Super Senior Citizens

In the Union Budget 2025, Finance Minister Nirmala Sitharaman introduced several changes to the income tax structure, particularly benefiting senior citizens (aged 60 years and above) and super senior citizens (aged 80 years and above).

1. Revised Income Tax Slabs under the New Tax Regime:

- For All Individuals (including Senior and Super Senior Citizens):

- Income up to ₹4,00,000: Nil

- ₹4,00,001 to ₹8,00,000: 5%

- ₹8,00,001 to ₹12,00,000: 10%

- ₹12,00,001 to ₹16,00,000: 15%

- ₹16,00,001 to ₹20,00,000: 20%

- ₹20,00,001 to ₹24,00,000: 25%

- Above ₹24,00,000: 30%

Note: These slabs are applicable under the new tax regime, which continues to be the default regime.

2. Enhanced Tax Rebate under Section 87A:

The rebate under Section 87A has been increased to ₹60,000. This means that individuals with a net taxable income up to ₹12,00,000 will not have to pay any income tax.

3. Increased Basic Exemption Limit:

The basic exemption limit has been raised from ₹3,00,000 to ₹4,00,000, providing additional relief to taxpayers.

4. Standard Deduction:

Taxpayers can continue to claim a standard deduction of ₹75,000 from salary income under the new tax regime.

5. No Changes in Deductions and Surcharge:

There are no changes in the existing deductions available under the new tax regime. The surcharge rates on income tax liability also remain unchanged for the financial year 2025-26.

These updates aim to provide financial relief and simplify the tax structure for senior and super senior citizens, ensuring a more comfortable post-retirement life.

Income Tax Slab for Senior Citizens and Super Senior Citizens: AY 2025-26

In India, income tax rules are different for senior citizens (60-80 years) and super senior citizens (80+ years). The government provides tax benefits to ease their financial burden.

Senior Citizen Age for Income Tax.

A person is considered a senior citizen for income tax if they are 60 years or older but below 80 years during the financial year.

A super senior citizen age is 80 years or more.

Income Tax Slab for Senior Citizens (60 to 80 years)

Let’s read these details!

Income Tax for Senior Citizens: Old Tax Regime (With Deductions & Exemptions)

| Annual Income Range | Income Tax Rate |

| Up to ₹3,00,000 | No Tax (0%) |

| ₹3,00,001 – ₹5,00,000 | 5% on income above ₹3,00,000 |

| ₹5,00,001 – ₹10,00,000 | ₹10,000 + 20% on income above ₹5,00,000 |

| ₹10,00,001 and above | ₹1,12,500 + 30% on income above ₹10,00,000 |

New Tax Regime (Default Regime – No Deductions)

| Annual Income Range | Income Tax Rate |

| Up to ₹3,00,000 | No Tax (0%) |

| ₹3,00,001 – ₹7,00,000 | 5% on income above ₹3,00,000 (No tax after rebate) |

| ₹7,00,001 – ₹10,00,000 | ₹20,000 + 10% on income above ₹7,00,000 |

| ₹10,00,001 – ₹12,00,000 | ₹50,000 + 15% on income above ₹10,00,000 |

| ₹12,00,001 – ₹15,00,000 | ₹80,000 + 20% on income above ₹12,00,000 |

| ₹15,00,001 and above | ₹1,40,000 + 30% on income above ₹15,00,000 |

Super Senior Citizen Tax Slab (80 years and above)

Let’s explore these ITR slabs!

Old Tax Regime (With Deductions & Exemptions)

| Annual Income Range | Income Tax Rate |

| Up to ₹5,00,000 | No Tax (0%) |

| ₹5,00,001 – ₹10,00,000 | 20% on income above ₹5,00,000 |

| ₹10,00,001 and above | ₹1,12,500 + 30% on income above ₹10,00,000 |

New Tax Regime (Default Regime – No Deductions)

| Annual Income Range | Income Tax Rate |

| Up to ₹3,00,000 | No Tax (0%) |

| ₹3,00,001 – ₹7,00,000 | 5% on income above ₹3,00,000 (No tax after rebate) |

| ₹7,00,001 – ₹10,00,000 | ₹20,000 + 10% on income above ₹7,00,000 |

| ₹10,00,001 – ₹12,00,000 | ₹50,000 + 15% on income above ₹10,00,000 |

| ₹12,00,001 – ₹15,00,000 | ₹80,000 + 20% on income above ₹12,00,000 |

| ₹15,00,001 and above | ₹1,40,000 + 30% on income above ₹15,00,000 |

Income Tax Deductions for Senior Citizens and Super Senior Citizens for AY 2026-2027

Let’s explore the tax advantages available on investments, payments, and incomes to senior citizens and super senior citizens.

Income Tax Deductions for Senior Citizens and Super Senior Citizens- New Tax Regime (Section 115BAC)

The new tax regime, introduced in Budget 2020, offers lower tax rates but removes several deductions and exemptions. However, some key benefits remain:

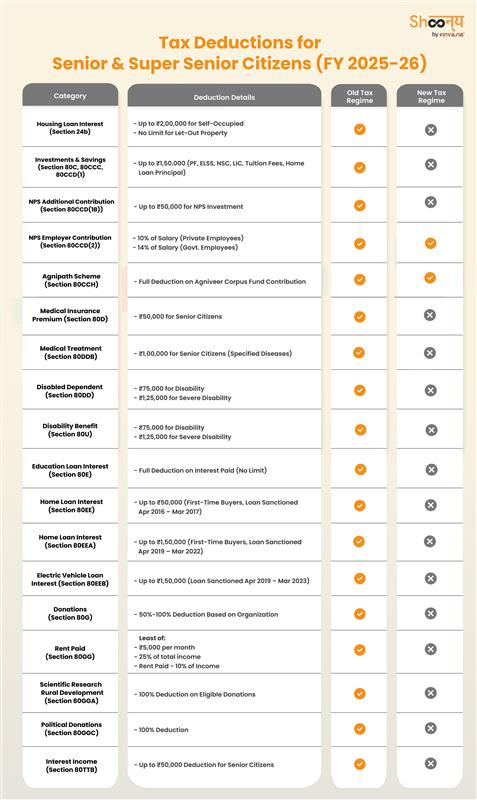

1. Housing Loan Interest (Section 24b)

- For rented/let-out property: There is no upper limit on the deduction for interest paid on home loans.

- For self-occupied property: The deduction is not available in the new tax regime.

2. Employer’s Contribution to Pension Scheme (Section 80CCD(2))

- Private sector employees can claim a deduction of up to 10% of their salary.

- Government employees can claim a deduction of up to 14% of their salary.

Income Tax Deductions for Senior Citizens and Super Senior Citizens- Old Tax Regime (Chapter VI-A Deductions)

The old tax regime allows multiple deductions under various sections. Taxpayers opting for this regime can claim benefits on home loans, insurance premiums, and more.

1. Home Loan Interest (Section 24b)

- For self-occupied property:

- Loan taken after April 1, 1999: Deduction up to ₹2 lakh.

- Loan taken before April 1, 1999: Deduction up to ₹30,000.

- For rented/let-out property: No limit on the deduction.

2. Investments Eligible for Tax Deductions

Several tax saving options for senior citizens and super senior citizens come under Section 80C (up to ₹1.5 lakh per year):

- Employees’ Provident Fund (EPF)

- Public Provident Fund (PPF)

- National Savings Certificate (NSC)

- Life Insurance Premiums

- 5-Year Fixed Deposit (FD) with Banks/Post Office

- Equity-Linked Savings Scheme (ELSS)

- Tuition Fees for Children

- Repayment of Principal on Home Loans

3. Additional Tax Benefits on Investments

- National Pension System (NPS) (Section 80CCD(1B)): Additional deduction of ₹50,000 over and above ₹1.5 lakh under Section 80C.

- Health Insurance Premiums (Section 80D):

- Self & family: Up to ₹25,000.

- For senior citizen parents: Additional ₹50,000.

- Interest on Education Loans (Section 80E): Full deduction on interest paid for higher education loans.

Tax Benefits on Incomes

Apart from investments, certain incomes also enjoy tax benefits:

- Agricultural Income: Fully exempt under Section 10(1).

- Interest on Savings Account (Section 80TTA): Up to ₹10,000 deduction.

- Senior Citizens’ Interest Income (Section 80TTB): Up to ₹50,000 deduction.

ITR Form For Senior Citizens and Super Senior Citizens

Exemption from Filing Income Tax Returns – Section 194P

ITR for Senior citizens aged 75 years and above may be exempted if they meet the following conditions:

- The individual must be 75 years or older.

- The individual must be a Resident in India for the previous year.

- The individual should have only pension income and interest income, and the interest should be from the same bank where the pension is received.

- The individual must submit a declaration to the specified bank.

- The bank must be a ‘specified bank’ notified by the Central Government. The bank will deduct TDS (Tax Deducted at Source) after considering deductions under Chapter VI-A and rebate under Section 87A.

- Once TDS is deducted by the specified bank, the senior citizen will not be required to file an income tax return.

ITR Forms for Super Senior Citizens

| ITR Form | Applicable To | Eligibility & Key Points |

| ITR-1 (SAHAJ) | Resident Individuals (excluding Not Ordinarily Resident) | – Total income up to ₹50 lakh- Sources: Salary/Pension, One House Property, Other Sources (Interest, Family Pension, Dividend), Agricultural Income up to ₹5,000 |

| Not Eligible If: | – Director in a company- Holds unlisted equity shares- Has assets or signing authority outside India- Has income from foreign sources- Tax deducted u/s 194N- Deferred tax on ESOP- Total income exceeds ₹50 lakh | |

| ITR-2 | Individuals & Hindu Undivided Families (HUF) | – No business or professional income- Not eligible for ITR-1 |

| ITR-3 | Individuals & HUF | – Income from Business or Profession- Not eligible for ITR-1, ITR-2, or ITR-4 |

| ITR-4 (SUGAM) | Individuals, HUFs & Firms (excluding LLPs) | – Total income up to ₹50 lakh- Income from Business/Profession computed on a presumptive basis (u/s 44AD/44ADA/44AE)- Other sources: Salary/Pension, One House Property, Interest, Family Pension, Dividend, Agricultural Income up to ₹5,000 |

| Not Eligible If: | – Director in a company- Holds unlisted equity shares- Has assets or signing authority outside India- Foreign income- Deferred tax on ESOP- Total income exceeds ₹50 lakh |

Other Important ITR Forms for Senior & Super Senior Citizens

| Form | Submitted By | Purpose |

| Form 15H | Resident Individuals (60 years or more) | Declaration to avoid TDS deduction on interest income |

| Form 12BB | Employees | Claims for tax deductions (HRA, LTC, interest on loan, tax-saving investments) |

| Form 16 | Employer to Employee | Details of salary, deductions, and TDS for tax filing |

| Form 16A | Deductor to Deductee | Quarterly TDS certificate for income other than salary |

| Form 26AS | Issued by Income Tax Dept. | Summary of TDS, tax payments, demand/refund details |

| AIS (Annual Information Statement) | Issued by Income Tax Dept. | Comprehensive tax details including TDS, SFT transactions, GST information |

| Form 10E | Employees | Claiming tax relief u/s 89(1) for arrears/advance salary, gratuity, pension commutation |

| Form 67 | Taxpayer | Declaring foreign income and claiming Foreign Tax Credit |

| Form 3CB-3CD | Taxpayers with audited accounts (u/s 44AB) | Audit report for business income, submitted one month before ITR due date |

| Form 3CEB | Taxpayers with international/specified domestic transactions | Transfer pricing audit report (u/s 92E), submitted one month before ITR due date |

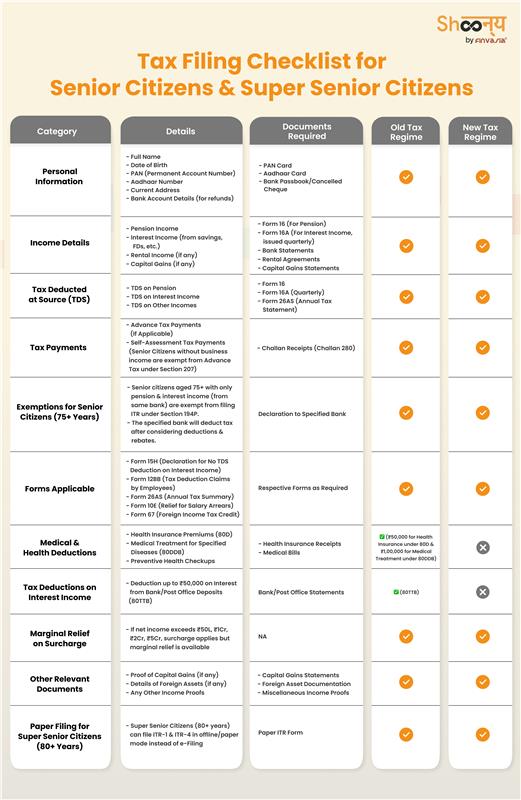

ITR Filing Checklist for Senior Citizens and Super Senior Citizens

Before filing your Income Tax Return (ITR), you must ensure you have all the necessary documents and details ready. You must always use an online income tax calculator to get an approximate idea beforehand.

This checklist will help senior citizens and super senior citizens avoid errors while filing their returns.

How to File ITR for Super Senior Citizens and Senior Citizens

Filing an Income Tax Return (ITR) is a mandatory process for senior citizens (60-80 years) and super senior citizens (80+ years) whose annual income exceeds the tax exemption limit.

If you want to know how to file income tax return online for Super Senior Citizen, you need to follow these steps to complete your ITR filing smoothly.

Step 1: Register on the Income Tax e-Filing Portal

- Visit the Income Tax Department’s e-Filing website: www.incometax.gov.in

- Click on ‘Register’ if you are a first-time user.

- Enter your PAN (Permanent Account Number), which will act as your User ID.

- Provide your mobile number and email ID for verification.

- Create a secure password and complete the registration process.

If already registered, log in using your PAN, password, and captcha code.

Step 2: Choose the Correct ITR Form

- ITR-1 (Sahaj) – For pensioners and senior citizens with income from salary, one house property, interest income, or family pension, with a total income up to ₹50 lakh.

- ITR-4 (Sugam) – For senior citizens earning business or professional income under the presumptive taxation scheme.

Step 3: Link PAN with Aadhaar and Pre-Validate Bank Account

- Ensure your PAN is linked with Aadhaar to avoid processing delays.

- Pre-validate your bank account on the e-Filing portal to receive any tax refunds.

Step 4: Pre-Fill and Verify Income Details

- The portal will automatically fetch details like pension income, fixed deposit interest, TDS deductions, and other sources of income from Form 26AS.

- Carefully review and edit the pre-filled information, if necessary.

If you have rental income, capital gains, or any other income, enter the details manually.

Step 5: Select the Tax Regime

- The New Tax Regime (default option) offers lower tax rates but does not allow deductions.

- If you prefer to claim deductions under 80C, 80D, and 80TTB, opt for the Old Tax Regime.

To opt for the Old Tax Regime, select “Yes” in the Filing Section of the ITR form.

Step 6: Claim Deductions (For Old Tax Regime Users)

If you have opted for the Old Tax Regime, claim eligible deductions:

- Section 80C – Investments in PPF, Senior Citizen Savings Scheme (SCSS), ELSS, 5-year Fixed Deposits

- Section 80D – Deduction of up to ₹50,000 on health insurance premiums

- Section 80TTB – Deduction of up to ₹50,000 on interest income from savings and fixed deposits

- Section 80G – Tax benefits for donations made to charitable institutions

Ensure all deductions are correctly entered before proceeding.

Step 7: Calculate Tax and Pay Any Pending Amount

- Once all income details and deductions are entered, the portal will automatically calculate your tax liability.

- If any tax is due, pay it online using net banking, UPI, or a debit card before submitting the return.

- Download and save the tax payment receipt for your records.

Step 8: Review and Submit the ITR

- Double-check all details in your ITR form to ensure accuracy.

- Click on ‘Preview and Submit’ to verify your return.

- If everything is correct, click ‘Submit’ to complete the process.

Step 9: E-Verify Your ITR

E-verification is mandatory within 30 days of filing. You can verify your ITR through:

- Aadhaar OTP (Recommended)

- Net Banking

- Pre-validated Bank Account

- Digital Signature Certificate (DSC)

- Sending a signed ITR-V to CPC, Bengaluru (if not e-verified online)

If verification is not done within 30 days, your ITR will be considered invalid.

Step 10: Track Your ITR Status & Refund

- After successful submission, you will receive an Acknowledgment Number.

- Check your ITR status under ‘My Account > Refund/Demand Status’ on the e-filing portal.

- If you are eligible for a tax refund, it will be credited to your pre-validated bank account.

Common Mistakes to Avoid While Filing ITR for Senior Citizens

Filing your Income Tax Return (ITR) correctly can help you save money and avoid penalties. But many senior citizens make common mistakes that can lead to problems later.

Let’s go through some key errors to avoid while filing income tax for senior citizens and super senior citizens.

You can always use an income tax calculator to estimate tax liability based on income, deductions, and tax slabs.

1. Choosing the Wrong ITR Form

Selecting the correct form is crucial.

- For pension and interest income, Use ITR-1.

- For multiple income sources (like rent, capital gains, or business income) – Use ITR-2 or ITR-3.

Using the wrong form can lead to rejection or extra tax liability.

2. Forgetting to Report All Income

Many senior citizens forget to include:

Interest earned from fixed deposits (FDs)

Interest from savings accounts, senior citizen savings schemes (SCSS), or post office deposits

Rental income (if applicable)

Capital gains from selling shares, property, or mutual funds

Even if tax is already deducted (TDS), you must report the income.

3. Not Claiming Deductions Properly

Senior citizens get special tax benefits! Make sure you claim:

- Section 80C – Up to ₹1.5 lakh for PPF, SCSS, life insurance, etc.

- Section 80D – Health insurance premium deduction (₹50,000 for senior citizens).

- Section 80TTB – Up to ₹50,000 exemption on interest income.

Missing these deductions means paying extra tax!

4. Not Checking Form 26AS & AIS

Your Form 26AS and Annual Information Statement (AIS) show all tax deductions (TDS) and income sources. Mismatches can lead to tax notices.

Cross-check before filing to avoid errors.

5. Missing the ITR Deadline

Late filing means penalties and delayed refunds. File your ITR before July 31st to stay stress-free.

ITR for Super Senior Citizen: Assisted Filing

The Income Tax Department has made e-filing easier with features like a selection wizard, pre-filled ITRs, an offline utility, chatbot support, and step-by-step guides. If you need further assistance, you can add a Chartered Accountant (CA), e-Return Intermediary (ERI), or an Authorized Representative to help with filing.

Who Can Assist You?

1. Chartered Accountant (CA)

- A CA is a certified professional from the Institute of Chartered Accountants of India (ICAI).

- You can add a CA via the My CA service on the e-Filing portal.

- They can file statutory forms, e-verify documents, handle grievances, and register DSC.

2. e-Return Intermediary (ERI)

- ERIs are authorised to file ITRs and manage tax-related services.

- Three types of ERIs exist based on the way they process returns.

- You can add or remove an ERI through the My ERI service, or an ERI can add you with consent.

- Services include filing returns and refund requests, updating contact details, and more.

3. Authorized Representative

- If you cannot handle tax matters yourself, you can authorise someone to act on your behalf.

Examples:

- NRIs → Resident Authorized Person

- Foreign companies → Resident Agent

- Deceased taxpayer’s estate → Executor/Administrator

- They get limited or full access depending on the authorisation.

Benefits of Filing ITR for Super Senior Citizens and Senior Citizens

The super senior citizen tax slab provides additional exemptions, making tax planning even more beneficial.

Tax saving options for super senior citizens include deductions on medical expenses, interest income, and pension income. The benefits of filing ITR for super senior citizens also include easier access to financial services and eligibility for refunds.

If you have doubts, learning how to file tax returns and how to file ITR for super senior citizens is the right way to start!

The higher deduction on interest income under Section 80TTB has been increased from ₹50,000 to ₹1,00,000, allowing more tax-free earnings from deposits. Additionally, the enhanced standard deduction for pensioners has been raised to ₹75,000, effectively reducing taxable income.

Another major benefit is the tax-free withdrawals from the National Savings Scheme (NSS) for withdrawals made on or after August 29, 2024, ensuring liquidity without extra tax burden.

Income Tax for Senior Citizens and Super Senior Citizens: FAQs

No, super senior citizens are not fully exempt from income tax, but they get a higher exemption limit of ₹5 lakh under the old tax regime.

Senior citizens are individuals aged 60-79 years, while super senior citizens are those aged 80 years and above.

Super senior citizens can claim deductions like ₹50,000 under Section 80TTB for interest income and ₹50,000 under Section 80D for health insurance.

Under the old tax regime, senior citizens have a basic exemption limit of ₹3 lakh, while super senior citizens have ₹5 lakh.

Under the old tax regime, super senior citizens have a tax exemption limit of ₹5 lakh.

Income tax is calculated based on slabs, exemptions, and deductions. Super senior citizens have a higher basic exemption limit and additional deductions.

Super senior citizens can claim deductions like ₹50,000 on interest income (80TTB), ₹50,000 on health insurance (80D), and standard deductions from pension income.

Source- TheEconomicsTimes , Incometax.gov.in

______________________________________________________________________________________

Disclaimer: Investments in the securities market are subject to market risks; read all the related documents carefully before investing.

Explore Our Offerings

Stocks

Trade equities across NSE and BSE with zero delivery charges. Invest, hold or sell with a seamless experience.

Future & Options

Execute complex strategies with simple tools and real-time data.

IPOs

Apply to the latest IPOs in just a few taps. Stay updated and capture opportunities as they open.