September 18, 2025

September 10, 2025

July 3, 2025

January 10, 2025

Types of Bonds in India: Understanding Your Options Before You Invest

Author

Shoonya Team

When people think about investing, they usually think of stocks first. But not everyone is comfortable with constant market ups and downs. This is where bonds come in.

Bond investment works on a simple principle: you lend money to a company or government, and they pay you interest regularly, promising to return the full amount by a set date. There are different types of bonds in India, each with its own risk level, return potential, and purpose.

In this blog, understand the classification of bonds in the Indian market.

Bond Meaning

A bond is a fixed-income investment where you lend money to a government or company, and in return, they promise to pay you regular interest and return your original amount at a fixed time.

Key parts of a bond:

• Issuer: The borrower, such as a government or company

• Face value: The amount you invest

• Interest rate (coupon): The fixed income you earn

• Maturity date: When your money is returned

Example:

If you buy a ₹10,000 bond with 7 percent interest, you earn ₹700 per year until maturity, and then get ₹10,000 back.

Types of Bond Markets in India

In India, the bond market can be broadly categorised into two types: Primary market and Secondary market

1. Primary Market

In the primary market, new debt securities are initially issued and sold directly to investors. Investment banks play an essential role in facilitating the issuance of bonds in the primary market.

2. Secondary Market

The secondary market involves the trading of existing bonds. You can easily purchase and sell bonds in the secondary market through intermediaries such as brokers. The bond prices in the secondary market fluctuate based on factors such as economic conditions and supply & demand.

Let us take a look at the various types of bonds in India!

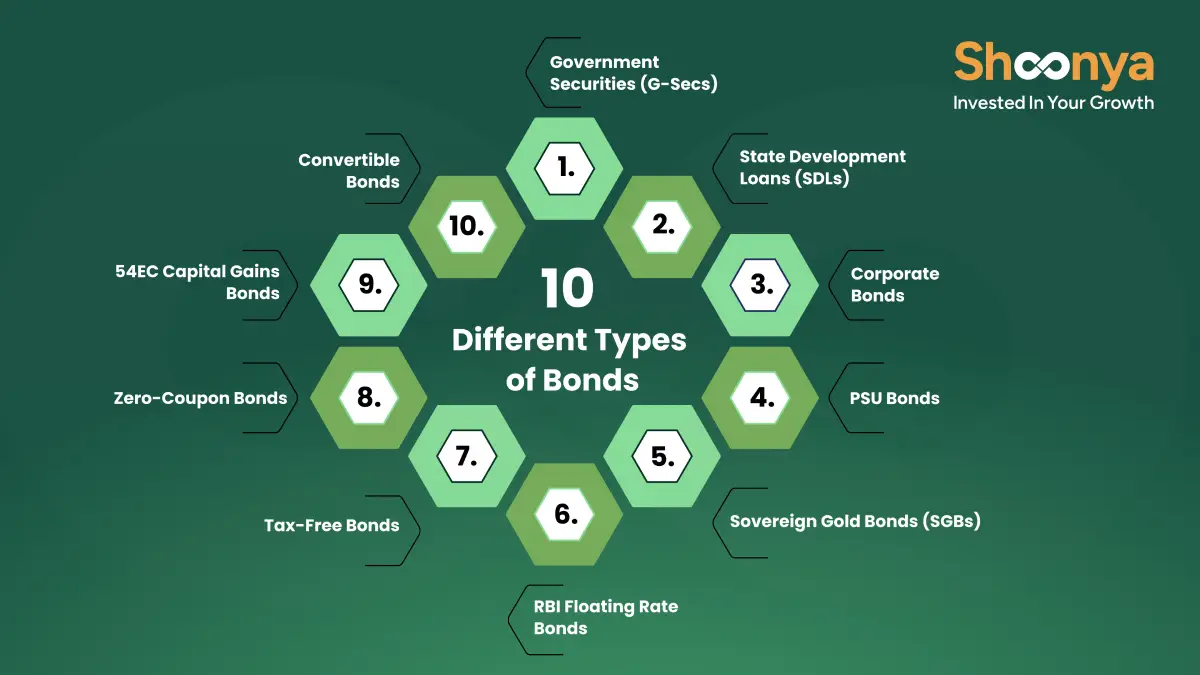

Types of Bonds in India

In India, key bond types include Government Bonds (safe, long-term), Corporate Bonds (higher yield, higher risk), and Tax-Free Bonds (issued for specific public infrastructure). They are classified by issuer (Government, PSU), interest structure (Fixed, Floating, Zero-Coupon), and special features (Convertible, Sovereign Gold Bonds).

Here are the most common bond types that will help you with meaningful portfolio diversification-

Government Bonds

The central or state governments issue government bonds to raise funds for various purposes. These could be liquidity crises or infrastructure development. These bonds are regarded as relatively safe investments as the government backs them.

Examples of government bonds in India are sovereign gold bonds, inflation-indexed bonds, and GOI savings bonds.

To make this clearer, here is a structured list of government bonds available in India based on tenure, interest type, and usage.

List of Government Bonds in Indian Market

| Bond Type | Issuer | Tenure | Interest Type | Key Feature |

| Treasury Bills (T-Bills) | Central Government | 91, 182, 364 days | No fixed interest (discounted issue) | Short-term, very low risk |

| Dated Government Securities (G-Secs) | Central Government | 5 to 40 years | Fixed or floating | Long-term stable income |

| State Development Loans (SDLs) | State Governments | 5 to 30 years | Fixed | Slightly higher returns than G-Secs |

| Sovereign Gold Bonds (SGBs) | Central Government | 8 years (exit after 5) | 2.5 percent + gold price | No need to hold physical gold |

| Floating Rate Savings Bonds (FRSB) 2020 | Central Government | 7 years | Floating (reset every 6 months) | Interest linked to NSC rates |

| Cash Management Bills (CMBs) | Central Government | Less than 91 days | Discount-based | Used for short-term cash needs |

| Special Securities (Oil Bonds, etc.) | Central Government | Varies | Fixed | Issued for specific purposes |

| Tax-Free Bonds | Govt-backed entities | 10 to 20 years | Fixed (tax-free interest) | No tax on interest income |

Treasury Bonds

These are government securities issued by the Central Government to raise funds for public projects. They’re considered a safe bet since they’re backed by the government.

Types of Treasury Bonds in India:

- Treasury Bills (T-Bills): These are short-term securities with maturities of 91 days, 182 days, and 365 days.

- Government Bonds (G-Secs): These are long-term securities with maturities that can range from 1 year to 40 years.

Corporate Bonds

Corporate bonds are debt instruments issued by companies to raise funds for business operations, expansion, or refinancing. When you invest, you are lending money to the company, and in return, you receive regular interest payments and your principal amount at maturity.

They usually offer higher returns than government bonds, but the risk depends on the company’s financial strength and credit rating.

Convertible Bonds

Convertible bonds are a special type of corporate debt. They pay interest like regular bonds. However, you can convert them into shares of the company’s stock at certain times. This conversion is usually up to you, the bondholder.

This feature provides the potential to participate in the company’s growth and benefit from stock price appreciation. Convertible bonds offer a unique combination of fixed income and equity exposure.

Zero-Coupon Bonds

Zero-coupon bonds, also known as discount bonds, do not pay regular interest. Rather, they are issued at a discount to their face value and redeemed at their full face value upon maturity.

The mere difference between the purchase price and the face value represents the investor’s return. Zero-coupon bonds are often favoured for capital appreciation.

Inflation-Linked Bonds

Inflation-linked bonds, as the name suggests, provide returns that are linked to inflation rates. The Reserve Bank of India (RBI) issues these bonds, and the interest payments adjust based on changes in the wholesale price index.

Investing in inflation-linked bonds can act as a hedge against rising inflation and help preserve purchasing power.

High-Yield Bonds

These are often called junk bonds. High-yield bonds are issued by companies with lower credit ratings. These offer higher yields to attract investors. The higher return compensates for the increased risk of default. If you’re willing to take on more risk, high-yield bonds might offer better returns.

Mortgage-backed securities (MBS)

Mortgage-backed securities are created by pooling together a bunch of mortgages and then issuing bonds based on this pool. The money you receive from these securities comes from the mortgage payments made by homeowners.

Because they’re backed by real estate, they generally carry less credit risk. Thus, they are a bit safer, though still subject to fluctuations in the real estate market.

Floating Rate Bonds

Floating rate bonds have interest rates that adjust periodically based on a reference rate, like the Reserve Bank of India’s repo rate. This means that the interest payments on this type of bond change with respect to market interest rates.

This feature helps protect investors from interest rate risk because the bond’s rate moves in line with market rates.

Callable Bonds

Callable bonds are defined as a category that gives the issuer the right to redeem the bonds before their maturity date. This feature offers the advantage of lower interest rates in the market. However, from an investor’s perspective, callable bonds do carry the risk of early redemption.

Your portfolio deserves more than just stocks.

Explore smarter bond investments with Shoonya today.

Features of Bonds

Bonds are a safe investment choice for investors.

Before you invest, it helps to understand what actually defines a bond. These are the core features that decide how much you earn, how safe it is, and how long your money stays invested.

Key features of bonds:

• Face value: This is the amount you invest and receive back at maturity

• Interest rate (coupon): The fixed or floating income you earn at regular intervals

• Maturity date: The date when your invested amount is returned

• Issuer: The entity borrowing money, such as the government or a company

• Credit rating: Indicates how reliable the issuer is in repaying the bond

• Yield: The actual return you earn, which can change based on market price

• Liquidity: How easily you can buy or sell the bond before maturity

Advantages of Bonds

Investment in bonds in India offers you several advantages:

- Stable Income: They provide regular interest payments.

- Lower Risk: Bonds are generally less volatile than stocks.

- Predictable Returns: Bonds usually have a fixed term and interest. They are suitable for someone who wishes to make safe investments.

- Diversification: Adding types of bonds to your investment portfolio can help balance out the risky investments.

Limitations of Bonds

Bonds are considered stable, but they are not risk-free. Investment in bonds in India is suitable for investors looking for stable and predictable returns.

Key limitations of bonds:

• Interest rate risk: When interest rates rise, existing bond prices fall, which can lead to losses if you sell before maturity

• Inflation risk: If inflation is higher than the bond’s return, your real earnings lose value over time

• Credit risk: There is always a chance that the issuer may fail to pay interest or repay the principal

• Liquidity risk: Some bonds are not actively traded, making it difficult to sell them quickly

• Reinvestment risk: When bonds mature or are redeemed early, you may have to reinvest at lower interest rates

• Limited returns: Bonds usually offer lower returns compared to stocks, which may not be ideal for long-term wealth creation

How to Invest in Bonds in India

You can invest in bonds in India through the RBI Retail Direct platform, stock brokers, or bond mutual funds and ETFs.

Simple steps to invest in bonds:

• Complete your KYC: Ensure your PAN, bank account, and demat account are active.

• Choose where to invest: You can invest through the RBI Retail Direct platform for government bonds, or use stock brokers and online platforms for corporate bonds.

• Evaluate the bond: Check the credit rating, interest rate, and maturity period before investing.

• Understand the returns: Look at both the coupon rate and the overall yield to know what you will actually earn.

• Place your investment: Select the bond on your platform and complete the purchase.

• Track your investment: Monitor interest payments and market value, especially if you plan to sell before maturity.

You can invest in bonds with Shoonya at zero brokerage. Open an account today!

Types of Bonds in India – FAQs

The most popular types of bonds include government bonds, corporate bonds, municipal bonds, and treasury bonds.

As of 2026, the RBI Floating Rate Savings Bond offers an interest rate of 8.05 percent per annum for the period from 1 January 2026 to 30 June 2026. The rate is linked to the National Savings Certificate and is revised every six months.

The five types of bonds are Government Bonds, Corporate Bonds, Zero-Coupon Bonds, Tax Saving bonds and Convertible Bonds.

The 7 types of bonds in India are Government Bonds, Corporate Bonds, Convertible Bonds, Zero-Coupon Bonds, Inflation-Linked Bonds, RBI Bonds, and Sovereign Gold Bonds.

Bonds in India vary by the issuer (government, PSUs, corporates), tenure (short to long-term), coupon (fixed, floating, etc. and security.

Fixed Deposits are safer with guaranteed returns, while bonds may offer higher returns but come with some risk. The better option depends on your risk level and financial goals.

Only specific tax-free bonds issued by government-backed entities such as NHAI, PFC, and REC provide interest income that is completely exempt under Section 10(15) of the Income Tax Act. Regular corporate and government bonds are taxable, with interest added to your income and taxed as per your slab.

Bonds can be identified based on the issuer (government or corporate), maturity period, interest type (fixed or floating), and credit rating. Common types include government bonds, corporate bonds, convertible bonds, and zero-coupon bonds.

The three most common types are government bonds, corporate bonds, and municipal bonds, each with different risk and return levels.

Source: SEBI

Disclaimer: This content is for education and awareness purposes only and should not be considered investment advice or a recommendation. Investments in securities markets are subject to market risks. Read all the related documents carefully before investing.

Explore Our Offerings

Stocks

Trade equities across NSE and BSE with zero delivery charges. Invest, hold or sell with a seamless experience.

Future & Options

Execute complex strategies with simple tools and real-time data.

IPOs

Apply to the latest IPOs in just a few taps. Stay updated and capture opportunities as they open.