September 18, 2025

September 10, 2025

July 3, 2025

January 10, 2025

What is SIP| Basics, Types, and Key Insights

Author

Shoonya Team

As a trader, you know the market’s ups and downs can be stressful. If you’re looking for a simpler way to invest in the stock market without constant worry, SIP might be just what you need. What is SIP exactly?

Remember how our parents used to buy gold jewellery, not just for special occasions but as a way to save for the future? They knew that, over time, gold would grow in value. Investing through SIPs is like that but with a modern twist. Instead of buying gold, you’re putting away a little money regularly into mutual funds.

Wondering how SIP works?

It’s just like how a small gold bangle eventually becomes a family heirloom.

Many people delay investing, waiting for the ‘right’ time or fearing market ups and downs. But SIP in share market is more like planting small seeds regularly. However, it needs consistent care and time.

And the result?

These seeds grow into a lush garden of financial security.

And here’s the best part: you can kickstart your mutual fund investments with as little as ₹500. Sounds crazy? But it’s true.

In this blog, we’ll explore “what is SIP”, its benefits, the types of SIPs, and how to start SIP investments.

What is SIP Investment

SIP stands for Systematic Investment Plan. It’s a smart, disciplined, and convenient way to invest in mutual funds. Instead of investing a large sum all at once, you contribute a small amount regularly, usually every month.

With SIP in share market, you invest a fixed amount at regular intervals into a mutual fund scheme of your choice. This approach helps you accumulate wealth for the long term.

The best part?

You can make these regular deposits regardless of whether the market is bullish vs bearish.

How SIP Works?

Let us understand this with an Example.

Think of it like buying vegetables monthly.

Some days, tomatoes might be pricey, and you get fewer. On other days, they might be cheaper, and you get more. But because you buy regularly, over time, you end up with a good quantity.

SIP investment operates similarly.

Sometimes, you can buy more shares when prices are low and fewer when the prices are high. Over time, this strategy helps reduce the impact of market volatility and steadily grow your investment.

You can begin by choosing a mutual fund scheme that aligns with your financial goals. This is usually followed by setting up your SIP in mutual fund.

Now you can invest in both SIP and lump-sum mutual funds—at zero brokerage!

SIP in Share Market

How do You Invest in SIP?

SIP in mutual funds is a user-friendly investment. There are multiple types of SIP in share market that you can choose from!

1. Equity SIP

In Equity SIP, you invest your money in mutual funds that primarily invest in stocks or equities of companies.

Imagine you want to invest regularly in companies like Infosys, Reliance, or HDFC. Equity SIP allows you to do this by investing a fixed amount in these mutual funds every month.

2. Debt SIP

It involves investing in mutual funds that invest in fixed-income securities. This could include corporate bonds, government bonds, or other debt instruments.

If you prefer a more stable and less risky investment, Debt SIP might be suitable. It’s like lending money to the government or companies, and they pay you interest regularly.

3. Hybrid SIP

Hybrid SIP combines both equity and debt components in a single mutual fund. This provides a balanced approach, aiming to offer some growth potential while minimising risk.

Consider a mutual fund that invests part of your money in stocks for growth and part in bonds for stability. Hybrid SIP is like having a mix of both worlds to balance risk and return.

Enjoy a free demat account and zero AMC—make the smart switch today!

4. Tax-saving SIP (ELSS)

Tax-saving SIP, also known as Equity Linked Savings Scheme (ELSS), allows you to invest in equity mutual funds while offering tax benefits under Section 80C of the Income Tax Act.

Example

Suppose you want to save on taxes while aiming for long-term wealth creation. ELSS SIP lets you do this by investing in equity funds, and the invested amount is deductible from your taxable income.

5. Index SIP

Index SIP involves investing in mutual funds that aim to replicate the performance of a market index like Nifty or Sensex.

If you believe in the overall growth of the stock market and don’t want to pick individual stocks, Index SIP allows you to invest in a mutual fund that mirrors the performance of a market index.

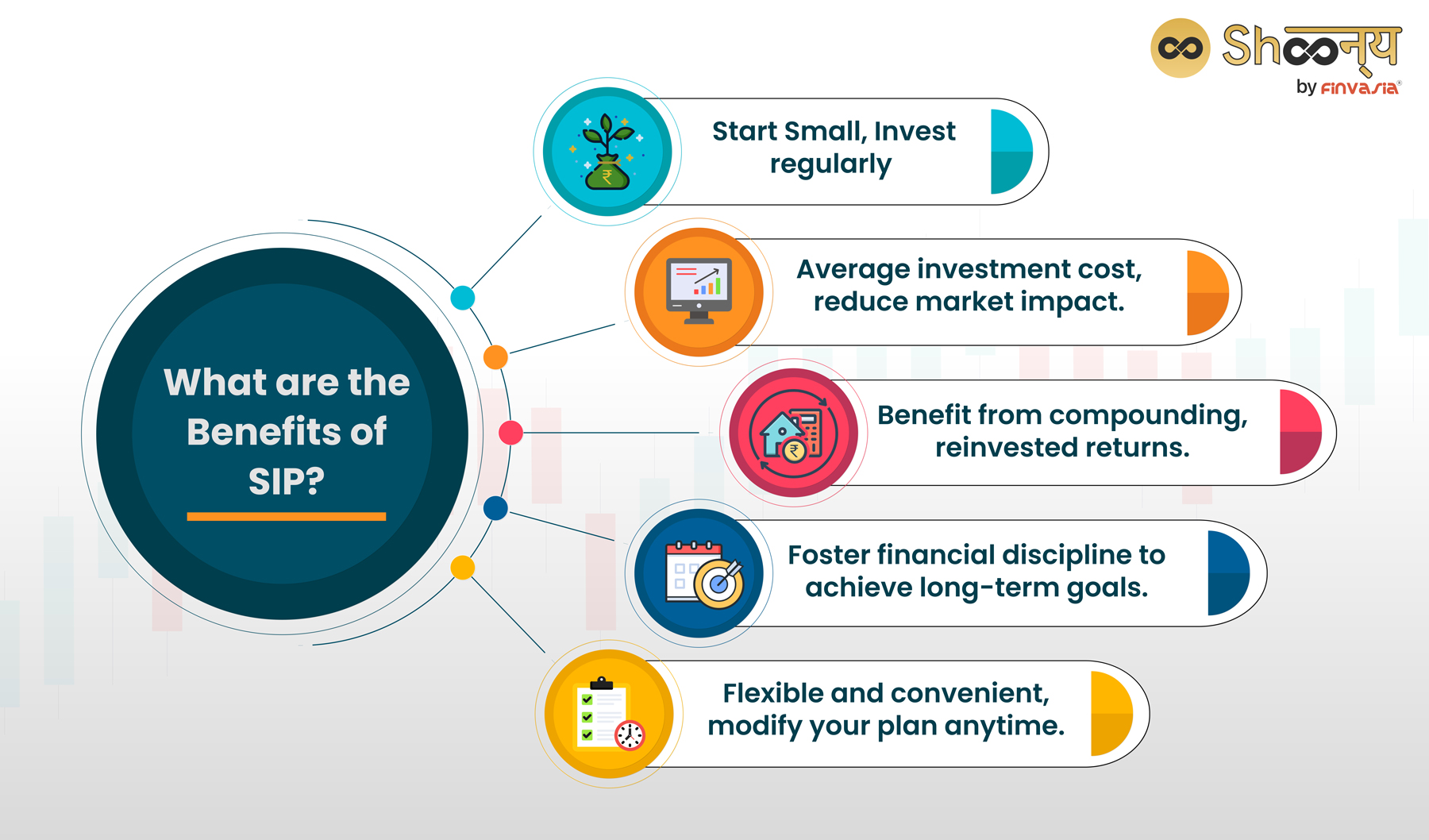

What are the Benefits of SIP?

Here are the benefits of SIP:

- SIP in mutual funds helps you invest regularly. You can turn saving and investing into a routine.

- You can begin with just a small amount, making it easy to start even if you don’t have a lot to invest.

- By investing regularly, you buy units at different prices. This helps reduce the impact of market ups and downs.

- SIPs invest at set intervals, so you don’t need to worry about guessing the best time to invest.

- You can change how much you invest and how often, based on your financial needs and goals.

- Once you set up an SIP, you can manage it online with minimal effort.

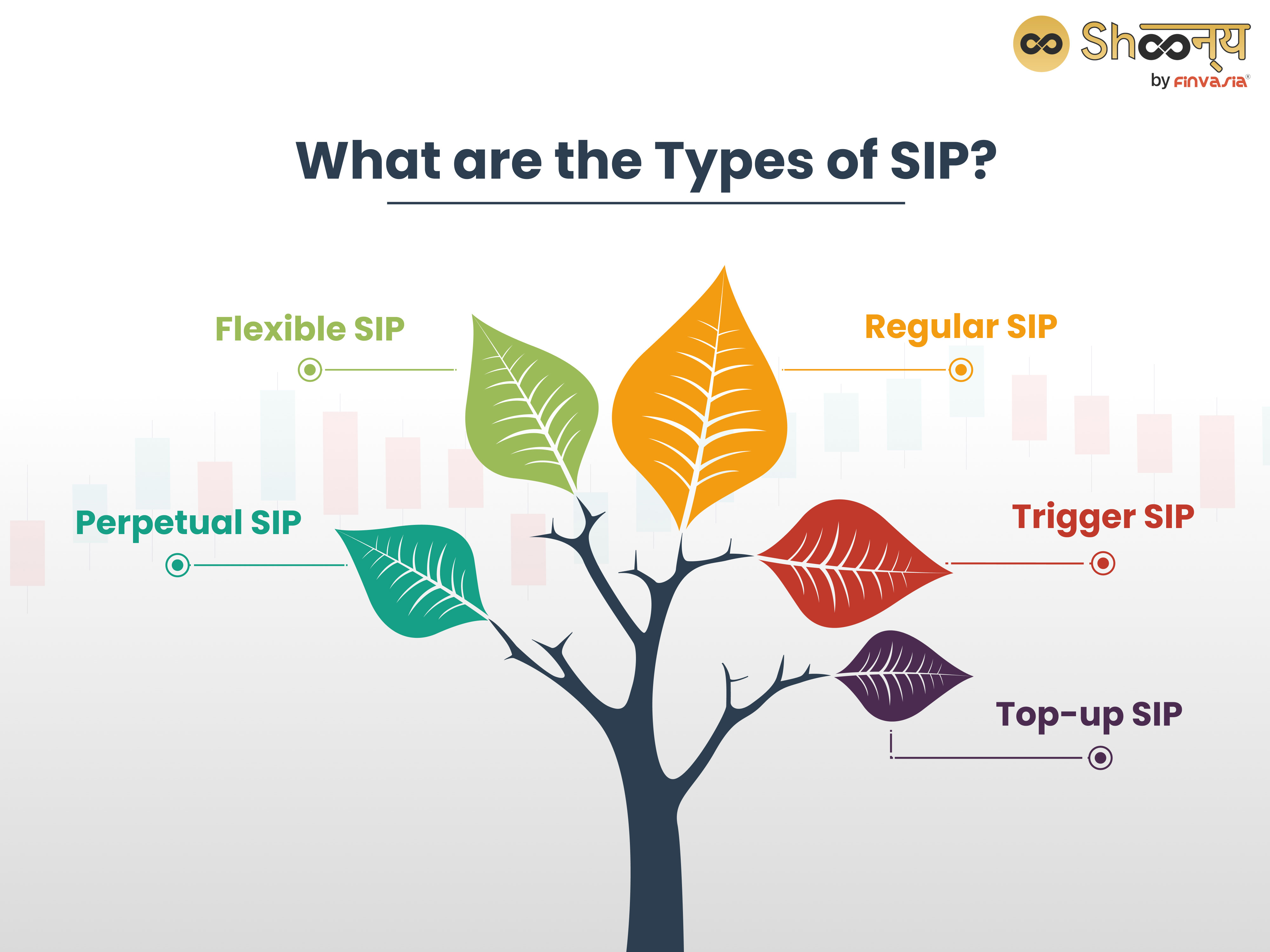

What are the Types of SIP?

There are five types of SIP in the share market.

- Regular SIP

This is the simplest type of SIP, where you invest a fixed amount at regular time intervals i.e. monthly, quarterly, or yearly. This helps you to accumulate a large corpus over time with small contributions.

So, imagine this as your go-to, regular investment routine. You decide to put ₹5,000 every month into an Equity Mutual Fund – a fixed amount, month after month.

Go for a Normal SIP if you’re into the whole “consistency is key” vibe.

- Trigger SIP

This allows you to set a trigger for your SIP mutual fund investment, such as a specific date, NAV level, or market index. When the trigger is met, your SIP amount is automatically invested in the mutual fund of your choice. This helps you to take advantage of favourable market movements and optimise your returns.

Opt for it when you want your investments to respond to specific market conditions without you constantly watching.

- Top-up SIP

This SIP investment allows you to increase your investment amount periodically, such as every year or every quarter. Thus, you can invest more when your income increases and also benefit from the power of compounding.

It’s like giving your investments an annual bonus.

When you foresee your income getting a boost over the years, Top-up SIP is your friend. Opt for it to level up your investments gradually.

- Perpetual SIP

This type of SIP does not have a fixed end date and continues until you stop it. This helps you to stay invested for the long term and achieve your financial goals.

Perpetual SIP is like setting and forgetting but in a good way.

If you’re in for the long haul and don’t want the hassle of renewing your investment plan periodically, Perpetual SIP is the perfect SIP investment choice.

- Flexible SIP

This type of SIP allows you to change your investment amount or frequency according to your convenience or market conditions. You can increase or decrease your SIP amount or pause or resume your SIP as per your wish.

Flexibility is the name of the game here.

You can choose Flexible SIP if your income is a bit of a rollercoaster. Opt for it when you want to tweak your investment strategy based on how your finances are doing.

Wondering if there any Risk in SIP?

While SIPs are a great way to invest regularly and manage market volatility. However, it’s important to remember that they do carry some risks. The value of your investments can fluctuate with market conditions, so there’s no guarantee of returns. However, the long-term benefits often outweigh these risks, especially if you stay invested and keep your goals in mind.

- Generally, equity funds are more risky but have higher returns, while debt funds are less risky but have lower returns.

- Hybrid or balanced funds are somewhere in between, offering a mix of risk and return.

Is SIP tax-free?

SIP is not tax-free, as it depends on the type of mutual fund you invest in and the duration of your investment.

The tax treatment of SIP is as follows:

Equity funds: In case you invest in equity funds through SIP and redeem your investment after one year, you have to pay a long-term capital gains tax of 10% on the gains that exceed Rs. 1 lakh in a financial year.

If you redeem your investment before one year, you must pay a short-term capital gains tax of 15% on the gains.

• Debt funds: In case you invest in debt funds through SIP and redeem your investment after three years, you have to pay a long-term capital gains tax of 20% with indexation benefit on the gains.

Indexation benefit means adjusting the cost of your investment with inflation, which reduces your taxable gains.

If you redeem your investment before three years, you have to pay a short-term capital gains tax as per your income tax slab on the gains.

• ELSS funds: By opting for Systematic Investment Plans (SIP) in Equity Linked Savings Schemes (ELSS), you become eligible for a tax deduction of up to Rs. 1.5 lakh as per Section 80C of the Income Tax Act.

However, you have to stay invested for at least three years, as ELSS funds have a lock-in period of three years.

The gains from ELSS funds are taxed as equity funds.

How to Start an SIP investment?

Starting a SIP investment is very easy and simple, and you can do it online or offline, as follows:

Start SIP in Mutual Funds Online

You can start an SIP investment online through Shoonya, which offers zero brokerage along with advanced trading tools, zero AMC and AI-powered insights!

How to Apply for SIP from Mobile Web (trade.shoonya.com):

- Go to Orders > Click on XSIP > Search for the mutual fund you want to invest in.

- If this is your first SIP with Shoonya, you need to create a Mandate ID first.

- Click on Create Mandate ID.

- Enter the Mandate amount (this is the limit for your SIP each day) and the validity date for your SIP investments.

- Click on Submit.

- You’ll receive a Mandate authentication link by email. It will take up to 24 hours for your bank to approve the Mandate.

Once your Mandate is approved, you can place your SIP order:

- Go to Orders > Click on XSIP > Search for the mutual fund you want.

- Click on XSIP, enter the SIP amount, and choose Fresh as the transaction type.

- Select the date for the SIP to be debited from your registered bank.

- After Mandate approval, it will auto-fill the Mandate ID.

- Choose Monthly for the frequency and enter the number of instalments (e.g., 24 instalments for a 2-year SIP).

You just need to register yourself, complete your KYC process, choose a mutual fund scheme, and set up a SIP mandate with your bank.

You can also track and manage your SIP investment online and make changes or withdrawals as needed.

How to Start SIP in Mutual Funds Offline

To start an offline SIP in a mutual fund, follow these steps:

1. Scheme Selection:

Choose a mutual scheme that aligns with your investment objectives.

Visit the fund house’s office.

2. Application Form:

Fill out the application form with your name, address, chosen scheme, SIP amount, and tenure.

3. KYC Formalities:

You must complete the KYC (Know Your Customer) formalities.

Fill out the relevant KYC-related form.

4. Document Submission:

You must submit the filled forms along with all the necessary documents.

5. Payment:

Pay the SIP amount as per your investment plan. You need to ensure the payment details are correct.

6. Confirmation:

Once you receive confirmation of payment receipt, you can obtain units of the selected schemes.

By following these steps, you can initiate an offline SIP and start investing in mutual funds through SIP.

How to Choose Mutual Funds for Your SIP

Picking the right mutual funds for your SIP is all about finding what fits your needs.

- Know Your Risk Tolerance:

- If you’re not a fan of taking risks, debt funds might be your best bet. They’re safer but offer lower returns.

- For those who don’t mind a bit of risk for potentially higher returns, equity funds are a good choice.

- If you like a balance, hybrid or balanced funds mix both types, giving you a blend of safety and growth.

- Think About Your Goals:

- Short-Term Goals (like a vacation or a new gadget)?

Debt funds are stable and easy to access. - Long-Term Goals (like saving for retirement or your child’s education)?

Equity funds could help you grow your money over the long haul. - Medium-Term Goals (such as buying a house)?

Hybrid or balanced funds might be just right, offering a mix of growth and stability.

- Short-Term Goals (like a vacation or a new gadget)?

- Check How the Fund Performs:

- Look for funds that have consistently done well compared to others in their category.

- Check their performance over various periods (1 year, 3 years, 5 years, and 10 years) to see if they’ve been steady and reliable.

Just a heads-up: while SIPs are a great investment tool, they’re not tax-free. The taxes you pay depend on the type of fund, how long you invest, and your earnings. So, make sure to weigh all these factors before jumping in.

When to Start Investing in SIP

Thinking about starting a Systematic Investment Plan (SIP)?

Here’s when it’s a good idea to start!

- Start Early: The sooner you start, the more you can benefit from compounding. This means your money has more time to grow.

- Stay Consistent: Regular investments help balance out market ups and downs, making your investment smoother.

- Align with Your Goals: It’s best to start an SIP when you have clear financial goals, like saving for retirement or your kids’ education.

Things to Keep in Mind Before You Start a Systematic Investment Plan (SIP)

Before you jump into a SIP, consider these factors:

- You must know what you’re saving for, whether it’s short-term or long-term.

- You must be aware of how comfortable you are with market changes.

- You need to know how long you plan to invest your money.

- You must choose funds that fit your risk level and financial goals.

- Check the fees or expense ratios associated with the funds.

- Set an SIP amount that fits your budget.

- Regularly review your investments to make sure they’re on track with your goals.

Conclusion

By investing small amounts regularly in SIPs, you can grow your wealth steadily over time. Starting early and staying consistent with SIPs can help you achieve long-term financial security, even with modest investments.

FAQs | SIP Investments

SIP (Systematic Investment Plan) and FD (Fixed Deposit) are different ways to invest. SIP involves regularly investing a fixed amount. FD, on the other hand, requires a lump sum investment for guaranteed returns and capital preservation.

Yes, you can invest 1000 ₹ per month in SIP. Many mutual fund schemes allow SIP starting with a minimum amount of 500 ₹ or 1000 ₹ per month.

Yes, you can withdraw your SIP investments anytime, except when there’s a lock-in period, such as with tax-saving ELSS funds. However, you need to be aware of the potential exit load.

SIP and lumpsum are both suitable for mutual fund investments, depending on your affordability, risk tolerance, and market conditions. SIP is ideal for investing small amounts regularly, whereas lumpsum works well if you have a significant amount to invest for long time.

SIP, or Systematic Investment Plan, is a disciplined way to invest in mutual funds by contributing a fixed amount at regular intervals.

SIP stands for Systematic Investment Plan. It’s a way to invest a fixed amount regularly in mutual funds. This approach helps in building wealth over time by spreading your investments.

Unfortunately, no investment is 100% safe. SIPs carry some market risk because they invest in mutual funds, which can fluctuate in value based on market conditions.

Yes, SIPs do have risk. Since they invest in mutual funds, the returns can vary depending on the market’s performance. So, while SIPs can be a great way to invest regularly, it’s important to be aware of the potential for fluctuations in returns.

______________________________________________________________________________________

Disclaimer: Investments in the securities market are subject to market risks; read all the related documents carefully before investing.

Explore Our Offerings

Stocks

Trade equities across NSE and BSE with zero delivery charges. Invest, hold or sell with a seamless experience.

Future & Options

Execute complex strategies with simple tools and real-time data.

IPOs

Apply to the latest IPOs in just a few taps. Stay updated and capture opportunities as they open.